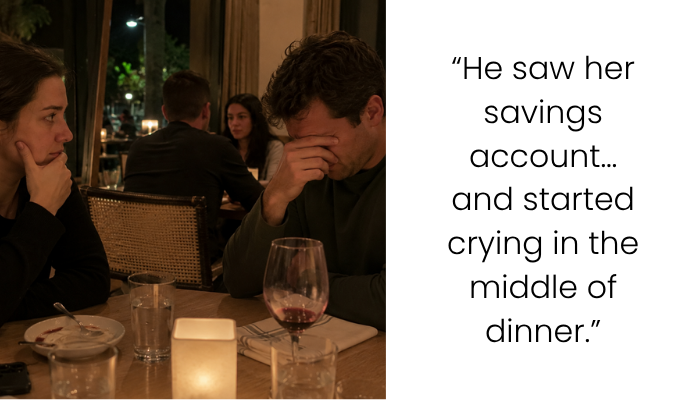

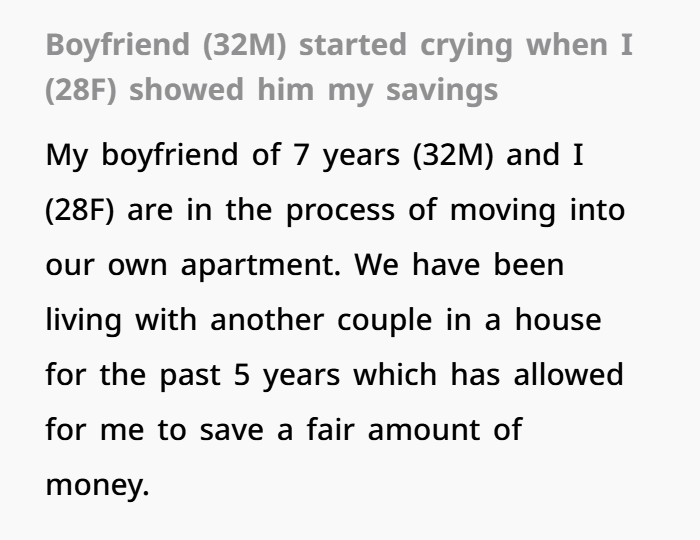

“My Boyfriend Cried When He Saw My Savings” — The Financial Reality Check That Changed Everything

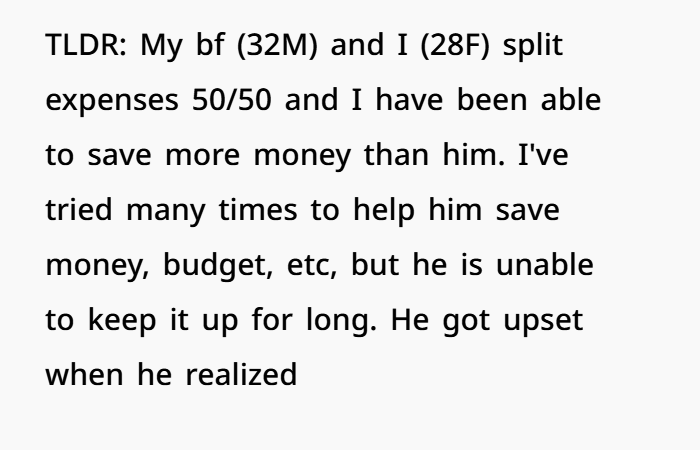

Money can become a difficult topic in relationships, especially when two people have different saving habits and financial goals. In this story, a woman shared what happened when she showed her boyfriend of seven years her savings account while they were planning to move into a more expensive apartment. Instead of feeling happy about their future plans, he became emotional and started crying during their dinner conversation.

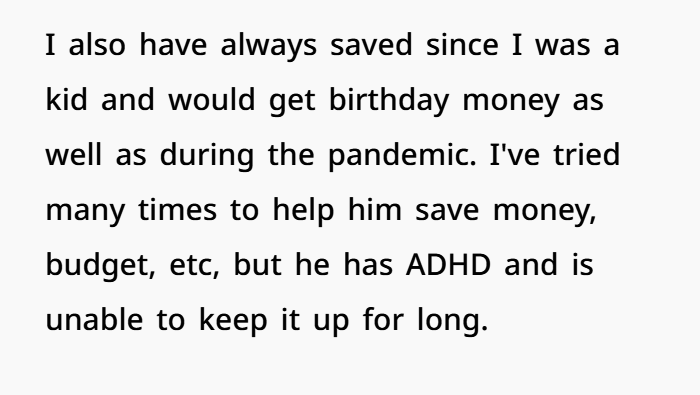

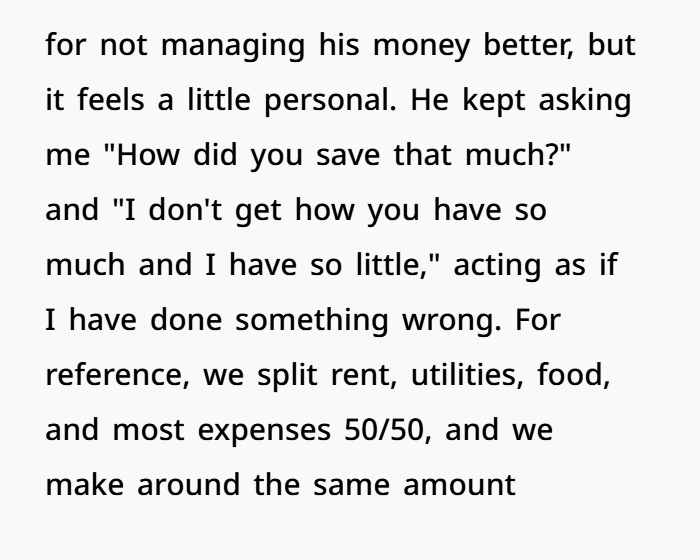

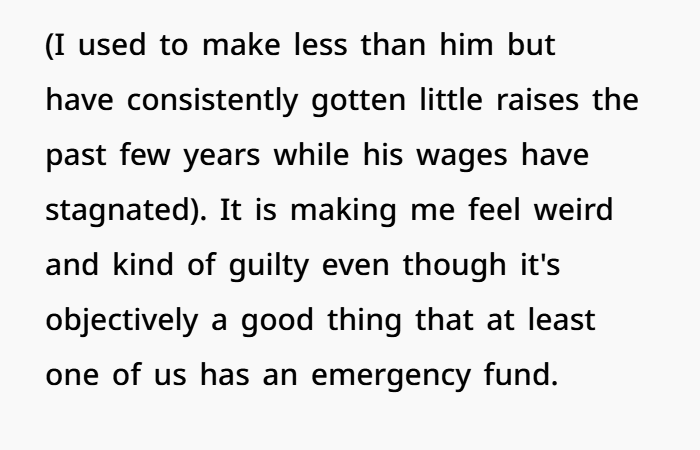

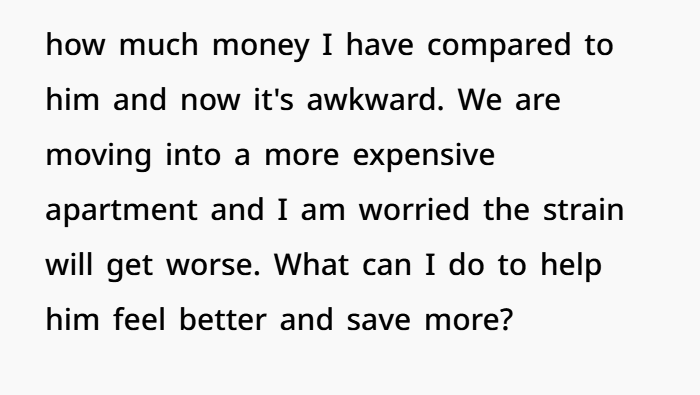

The situation was surprising because they had always shared expenses equally and earned similar incomes. They believed they had a similar financial situation, but the reality was very different. The woman had focused on budgeting, saving money, and building financial security over the years. She was careful with spending and had clear long-term financial goals.

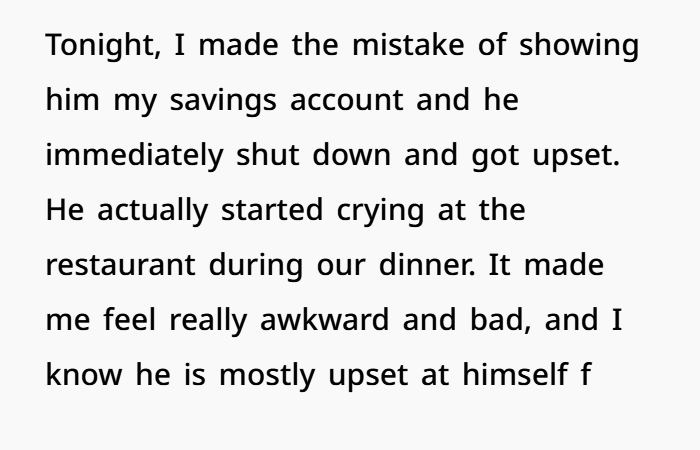

Her boyfriend, however, struggled with money management. He had difficulty controlling impulse spending and staying consistent with saving. He also dealt with ADHD, which made some daily financial habits more challenging for him. Seeing the difference between their savings accounts made him realize how much their financial habits had changed over time.

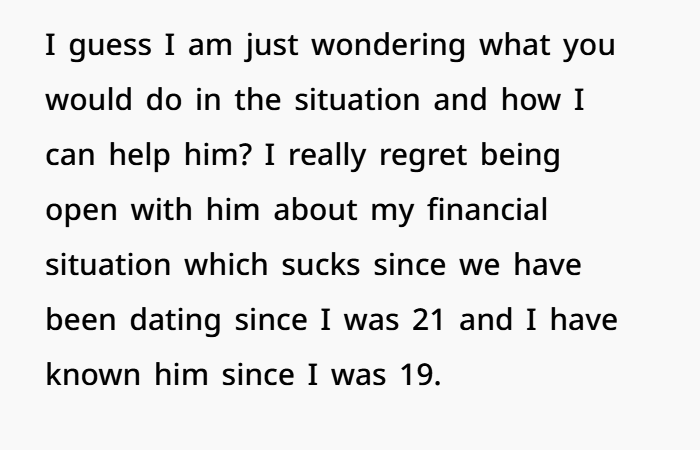

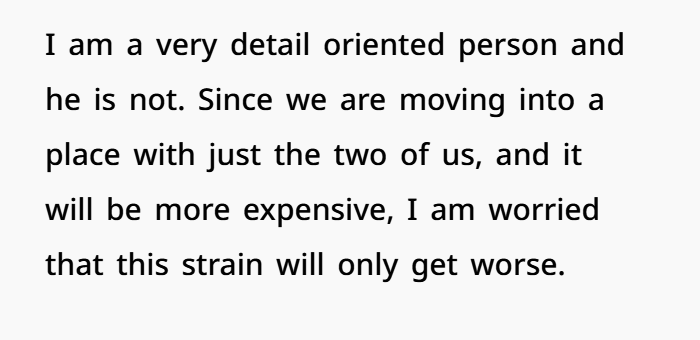

Now the couple is facing an important conversation about money, future planning, and shared expenses. The woman feels uncomfortable because she does not want her financial success to hurt his feelings, but she also understands that financial compatibility is important in a long-term relationship. The situation shows why couples should talk openly about budgeting, savings goals, debt, and financial responsibilities before making big decisions like moving in together.

When Money Differences Create Relationship Stress: A Story About Love, Budgeting, and Financial Compatibility

Money problems are one of the most common causes of stress in relationships.

Sometimes the problem is not the amount of money someone earns.

It is about how people manage money, plan for the future, and handle financial responsibilities.

This story may look like a disagreement about savings, but the deeper issue was about financial habits, confidence, trust, and whether two people have similar goals for the future.

The Real Meaning Behind Savings

When someone sees a large difference in savings between two partners, the emotional reaction is not always about the number itself.

Money often represents:

- Security

- Stability

- Independence

- Emergency protection

- Future planning

Having savings can make people feel prepared for unexpected situations like job loss, medical expenses, or major life changes.

So discovering that one partner has built strong financial security while the other is struggling can bring up difficult emotions.

It can create feelings of:

- Shame

- Stress

- Fear

- Disappointment

- Worry about the future

Similar Income Does Not Always Mean Similar Finances

One important detail in this situation was that both partners earned similar incomes.

This means the difference was not caused by one person having a much higher salary.

Instead, the gap likely came from different financial habits.

Over several years, small choices can create very different results.

Factors that affect financial health include:

- Saving consistently

- Managing expenses

- Avoiding unnecessary debt

- Planning ahead

- Building emergency funds

- Controlling impulse spending

Two people can start from a similar place and still end up in very different financial situations.

Understanding ADHD and Money Management

The ADHD factor is also important.

Some people with ADHD experience challenges with:

- Organization

- Time management

- Planning

- Impulse control

- Completing routine tasks

These challenges can make money management more difficult.

For some people, ADHD may contribute to problems like:

- Forgetting bills

- Delaying important tasks

- Impulse purchases

- Difficulty following budgets

However, understanding the reason behind a behavior does not remove the need to manage its impact.

A person can struggle with ADHD and still work toward better financial habits.

Both things can be true.

When Small Problems Become Bigger

The unpaid parking tickets mentioned in the story showed a larger pattern.

Small responsibilities can sometimes become bigger problems when they are repeatedly ignored.

For example:

- Unpaid bills

- Missed deadlines

- Delayed paperwork

- Avoiding financial planning

Over time, these issues can create stress for both people in a relationship.

The challenge is not only the money itself.

It is the feeling that one partner has to manage everything.

Why Financial Compatibility Matters

Couples do not need to have identical incomes or identical spending habits.

However, they usually need similar values around money.

Financial compatibility includes things like:

- Saving for goals

- Planning for the future

- Discussing spending openly

- Sharing responsibilities

- Creating realistic budgets

A relationship can become stressful when one person feels like the only responsible financial decision-maker.

Over time, that imbalance can create frustration and resentment.

Love and Money Problems Can Exist Together

One important part of this story is that the partner with more savings did not seem angry.

Instead, she appeared worried about the situation and concerned about his feelings.

That shows an important truth:

Financial differences do not automatically mean a relationship is unhealthy.

Many couples experience money challenges.

The key is how both people respond.

A healthy relationship requires:

- Honesty

- Respect

- Teamwork

- Willingness to improve

The Danger of Becoming the Financial Caretaker

Sometimes one partner slowly becomes responsible for everything.

They may become the person who:

- Creates the budget

- Pays attention to deadlines

- Organizes finances

- Solves money problems

- Plans for emergencies

Helping your partner is normal.

However, constantly managing another adult’s responsibilities can become exhausting.

A relationship works best when both people contribute.

Promises Are Important, But Actions Matter More

According to the story, the boyfriend wanted to improve his situation.

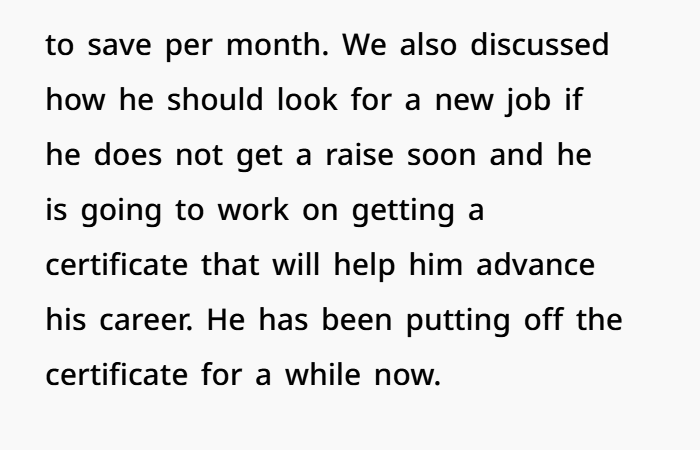

He talked about:

- Creating a budget

- Improving his income

- Learning new skills

- Building savings again

Those are positive steps.

However, long-term financial improvement comes from consistent actions.

Real change usually requires:

- New routines

- Better systems

- Regular saving habits

- Tracking expenses

- Financial education

Motivation can start change, but habits maintain it.

Helpful Financial Strategies for Couples

Couples facing similar challenges may benefit from practical steps such as:

- Creating a monthly budget together

- Setting shared financial goals

- Using automatic savings

- Tracking spending

- Building an emergency fund

- Having regular money conversations

For people with ADHD, external systems can be especially helpful.

Examples include:

- Budgeting apps

- Automatic payments

- Spending alerts

- Calendar reminders

- Professional financial guidance

The goal is to create systems that make success easier.

Protecting Your Own Financial Future

It is also important for both partners to protect their own financial stability.

Healthy financial boundaries may include:

- Maintaining personal savings

- Discussing major purchases together

- Avoiding taking on unnecessary debt

- Understanding shared financial responsibilities

Supporting someone does not mean losing your own financial security.

A Turning Point for the Relationship

This situation does not automatically mean the relationship cannot work.

It may actually become an opportunity for growth.

The important question is whether this emotional moment leads to real change.

Will new habits continue?

Will responsibilities become more balanced?

Will both partners work together toward a shared future?

Those answers matter more than one difficult conversation.

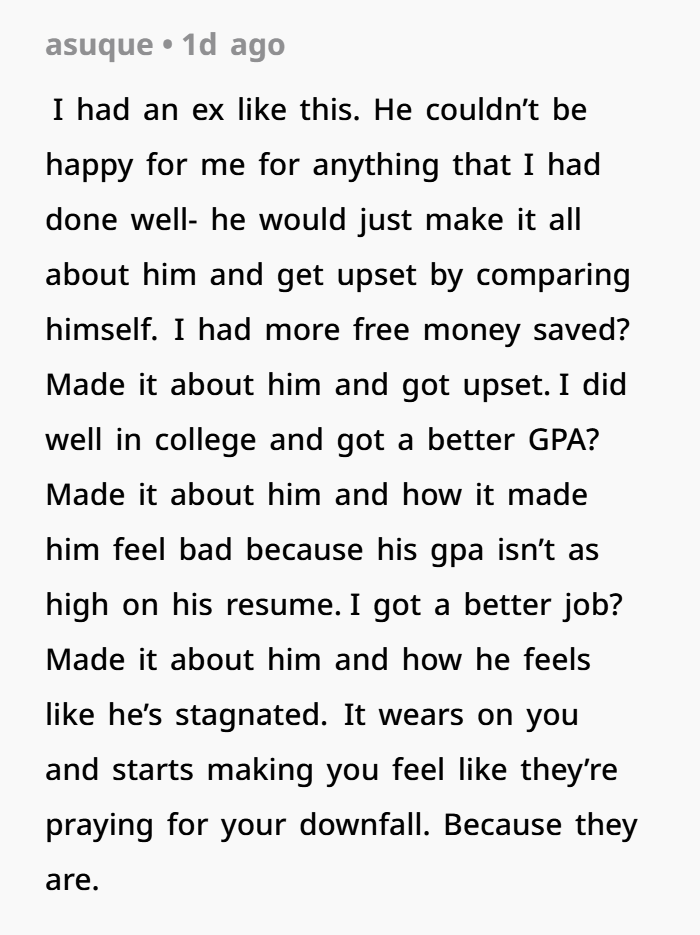

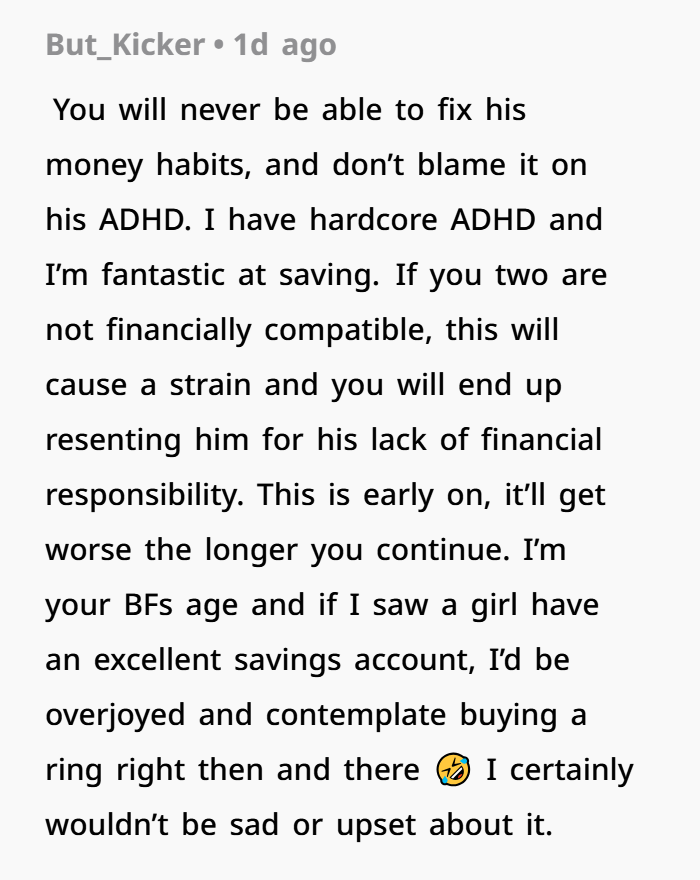

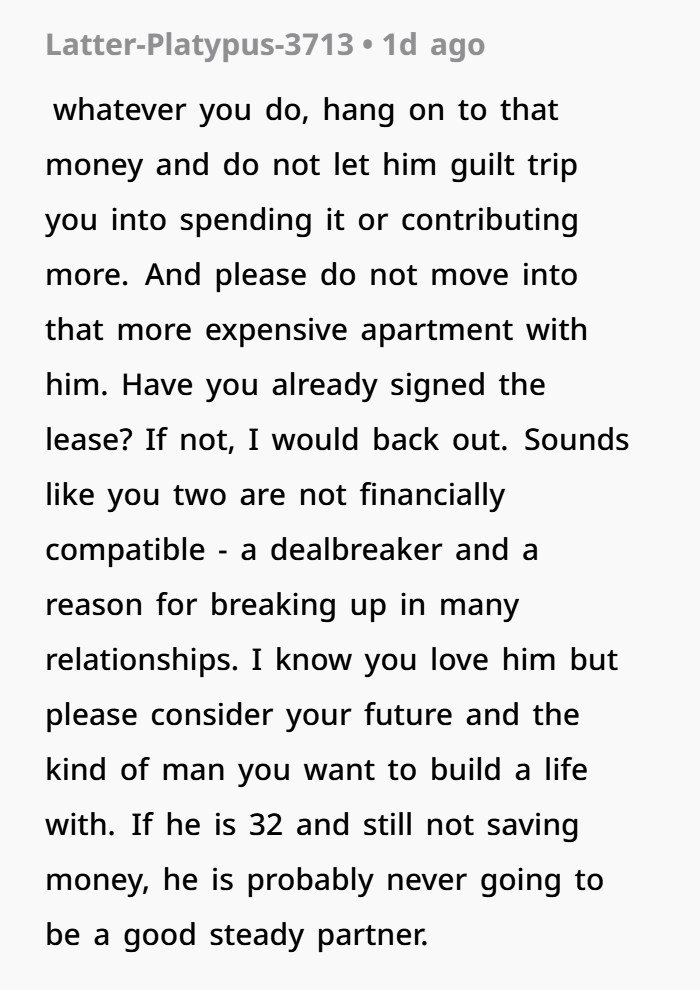

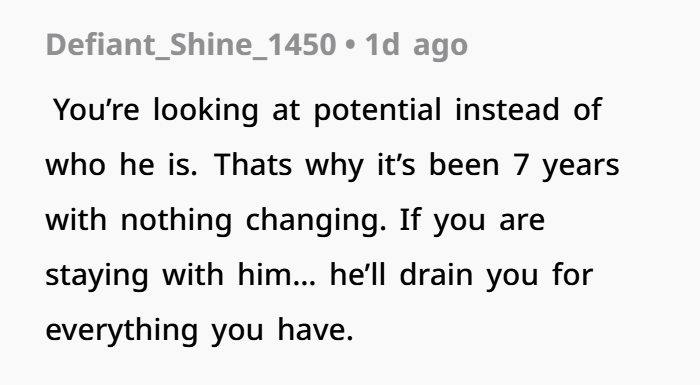

Readers had plenty of thoughts to share, and the woman replied to some of their comments along the way

Final Thoughts

This story was not only about a savings account.

It was about trust, responsibility, and building a stable future together.

Money is an important part of relationships because it affects security, choices, and long-term plans.

Two people can love each other deeply and still need to work on financial compatibility.

The strongest relationships are built when both partners are willing to learn, improve, and support each other while also taking responsibility for their own choices.