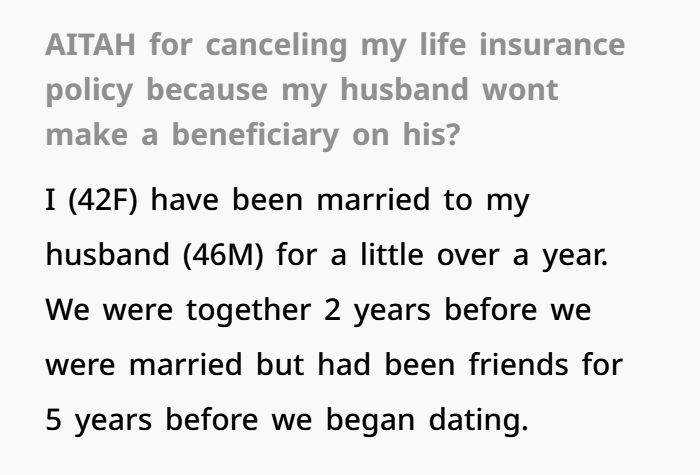

When My Husband Won’t Make Me a Beneficiary, I Made a Tough Choice

Financial planning can become complicated in blended families, especially when couples have children from previous relationships. A woman shared her experience after discovering that her husband did not name her as a beneficiary on his life insurance policy. This worried her because she had already experienced the loss of both parents and understood how difficult financial matters can become after someone passes away.

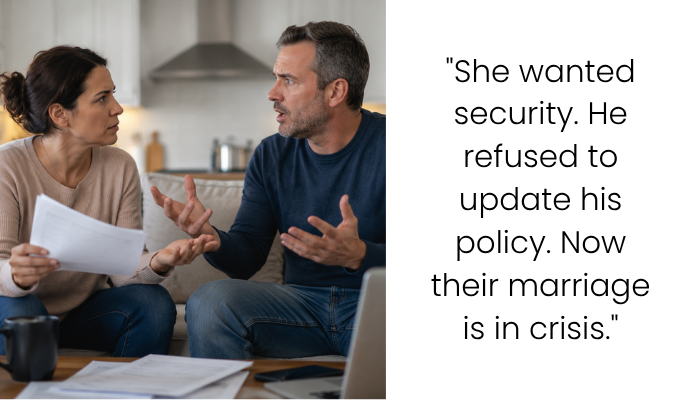

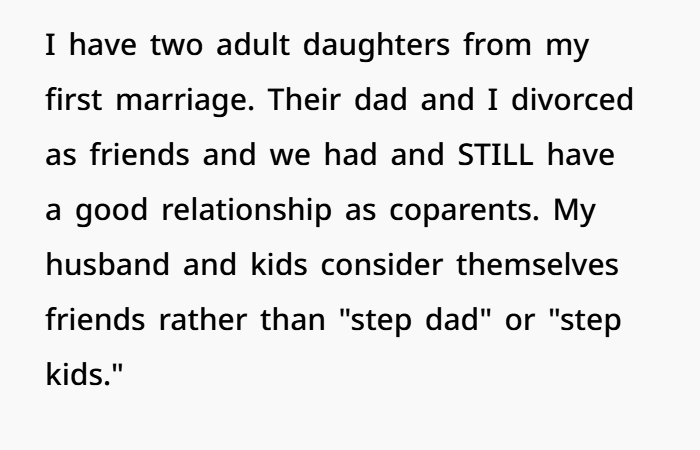

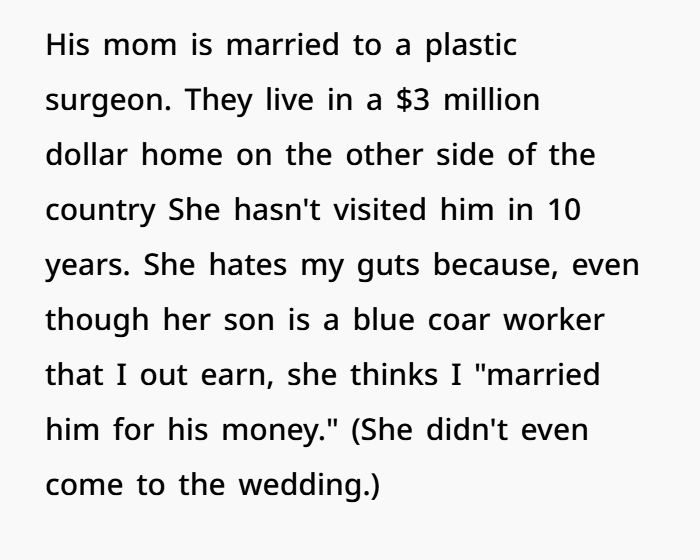

The woman wanted to make sure the people she cared about were protected. She created financial plans that included support for her husband and her two adult daughters from her previous marriage. When she asked her husband to make a similar plan, he refused and kept his mother as his only beneficiary, even though they had a distant relationship.

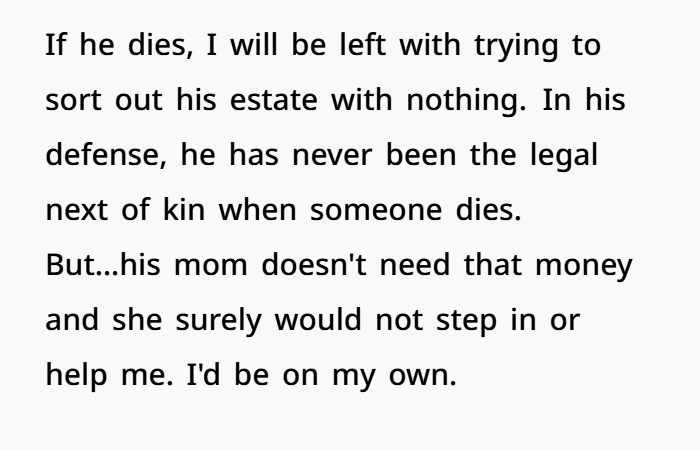

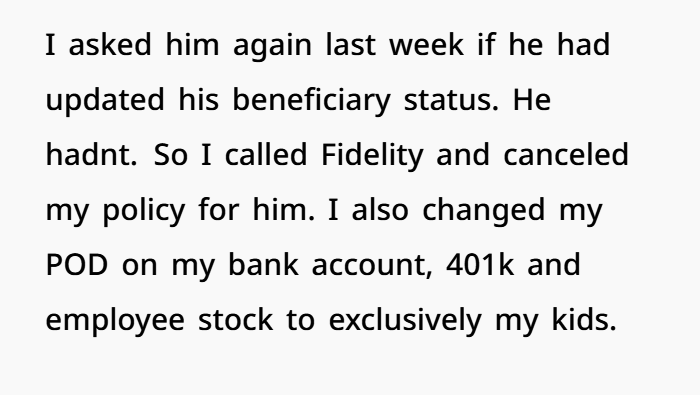

Feeling uncertain about her own financial security, the woman decided to change her plans. She removed her husband from some of her policies and accounts and chose to leave those benefits to her daughters instead. This decision created tension in their marriage, and her husband felt hurt by the change.

The situation shows why couples should have honest conversations about money, inheritance, and financial goals. Blended families often need careful planning to make sure everyone feels respected and secure. Clear communication, trust, and proper estate planning can help couples avoid misunderstandings and protect their loved ones.

Why Life Insurance Conversations Matter in Marriage

At first, this situation may look like a simple disagreement between a husband and wife. But the deeper issue is about financial security, trust, fairness, and planning for the future.

Life insurance is not only about money after someone passes away. It is also about protecting the people you love and making sure they are not left with unexpected financial problems.

This topic can become even more important in blended families, where couples may have children from previous relationships and different financial responsibilities.

Why the Wife Chose Life Insurance Planning

The wife had personal experience with losing family members and dealing with financial responsibilities after their deaths.

Handling estates, bills, and paperwork during a difficult emotional time can be overwhelming. Because of that experience, she wanted to make sure her own children would not face the same challenges.

Keeping life insurance for her adult daughters was not about fear. It was about preparation and financial planning.

Many financial experts recommend having a plan in place before a crisis happens. Life insurance can help families manage expenses, debts, and other financial responsibilities after a loss.

Protecting Both Partners in Marriage

After getting married again, the wife purchased a life insurance policy for her husband.

Her goal was to make sure he would have financial support if something happened to her. Since he earns less money than she does, she wanted to reduce the chance that he would struggle with expenses in the future.

This shows an important idea in financial planning: both partners in a marriage should think about each other’s security.

A strong financial plan usually considers both people, not just one person.

The Problem With Unequal Financial Protection

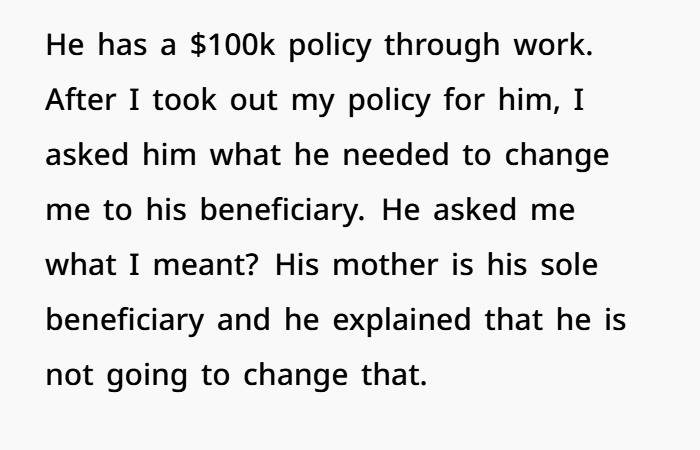

The conflict began when the wife asked her husband to name her as a beneficiary on his workplace life insurance policy.

He chose to keep his mother as the only beneficiary.

This decision created hurt feelings because the wife felt she was offering financial protection while not receiving the same support in return.

In marriage, money decisions can represent more than finances. They can also represent trust, partnership, and feeling valued.

Why Beneficiary Choices Matter

A life insurance beneficiary is the person who receives the policy payout after the insured person dies.

Choosing beneficiaries is an important part of estate planning. Many couples discuss these decisions together because they affect the family’s financial future.

Beneficiary decisions can become especially important in blended families because spouses and children may have different financial needs and expectations.

Every family situation is different, and people should consider speaking with a qualified financial advisor or estate planning professional for guidance.

Is Canceling the Policy a Reasonable Choice?

Some people may feel that canceling the life insurance policy was an emotional reaction.

Others may see it as setting a financial boundary.

From the wife’s perspective, she was asking why she should continue paying for a policy that protected someone who was not willing to provide similar protection for her.

Financial planning is not only about helping others. It is also about protecting your own future.

Creating financial boundaries can be an important part of responsible money management.

The Importance of Fairness in Marriage

Marriage often involves shared responsibilities and long-term planning.

Financial experts often encourage couples to discuss:

- Life insurance coverage

- Retirement planning

- Emergency savings

- Estate planning

- Debt management

- Future financial goals

When one partner feels financially protected while the other does not, it can create stress and resentment.

A healthy financial partnership requires open communication and mutual consideration.

Blended Families and Financial Planning

Blended families often require extra planning because there may be children, previous financial commitments, and different family relationships involved.

Parents may want to make sure their children are protected while also supporting their spouse.

There is no single solution that works for every family. The most important thing is creating a plan that is clear, fair, and discussed openly.

Having Better Money Conversations

Many financial disagreements are actually about emotions.

A conversation about life insurance may really be about questions like:

- “Do you care about my future?”

- “Are we working together as partners?”

- “Will we support each other during difficult times?”

Talking openly about these concerns can help couples understand each other better.

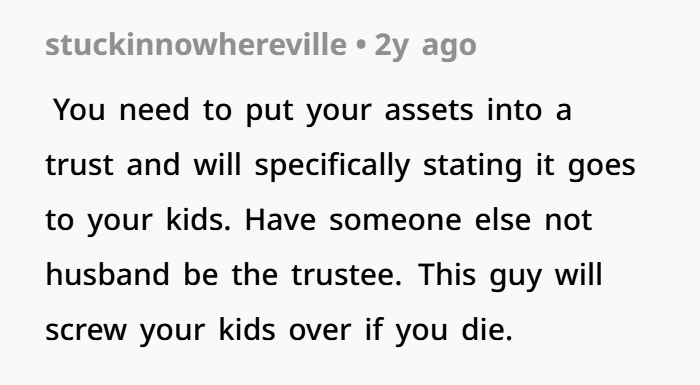

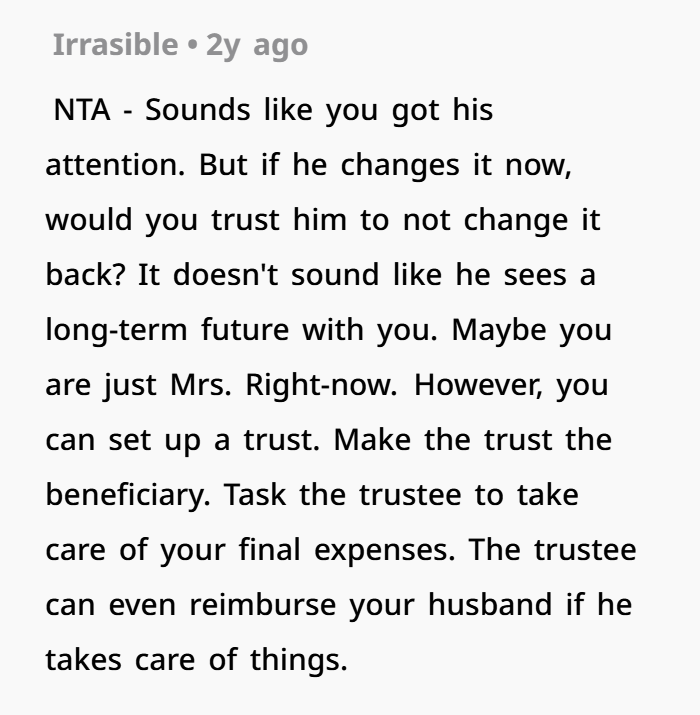

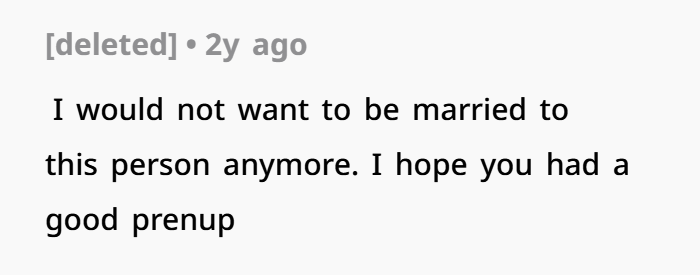

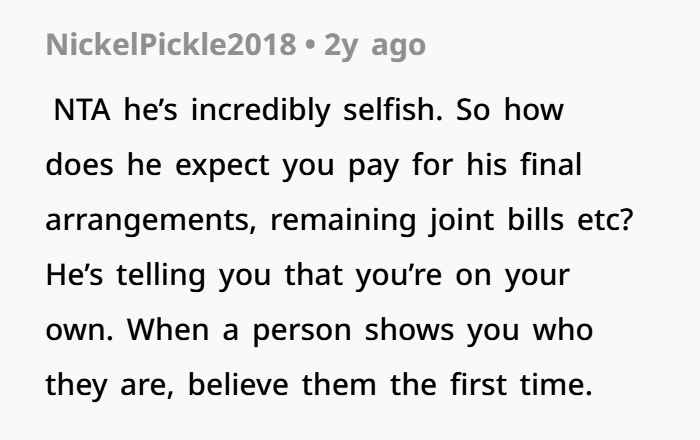

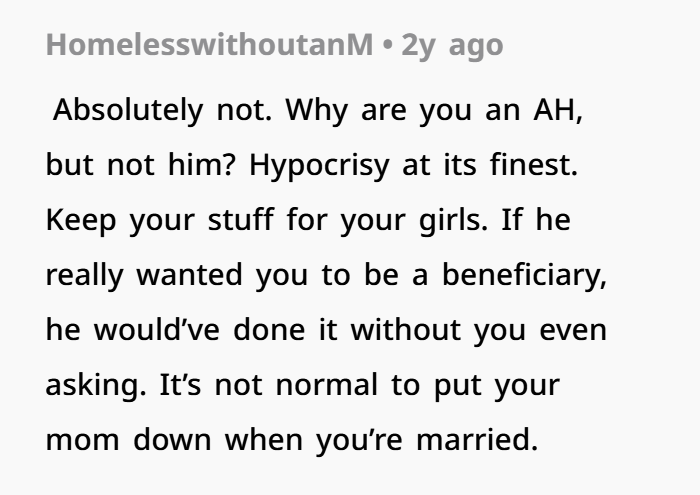

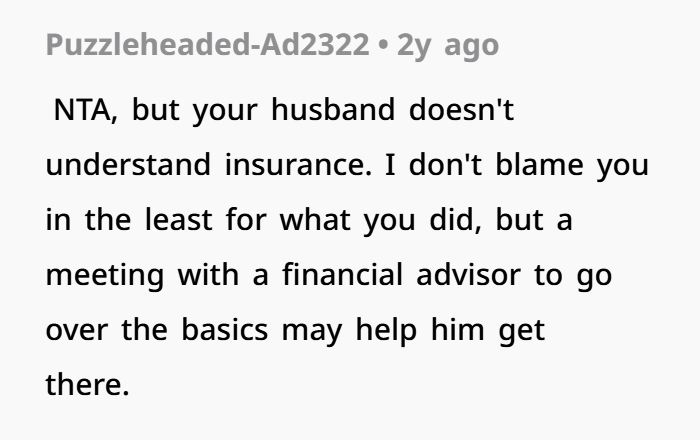

The Comments Are In

Final Thoughts

Life insurance is not only a financial product. It is a tool for protecting loved ones and preparing for unexpected events.

In a marriage, both partners deserve to feel secure and supported. Good financial planning requires honesty, teamwork, and respect.

The goal is not simply to decide who is right or wrong. The goal is to create a financial plan where both people feel valued and protected.