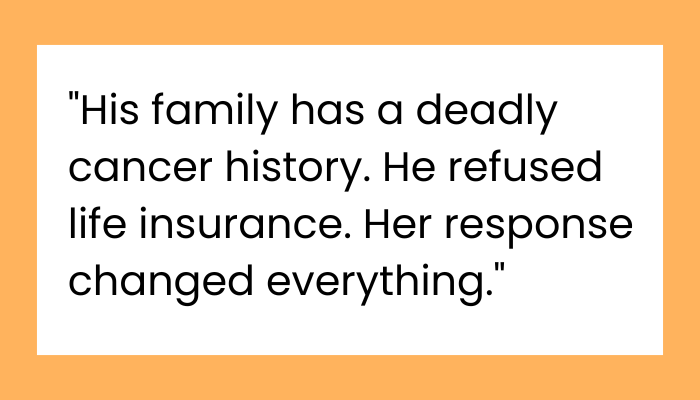

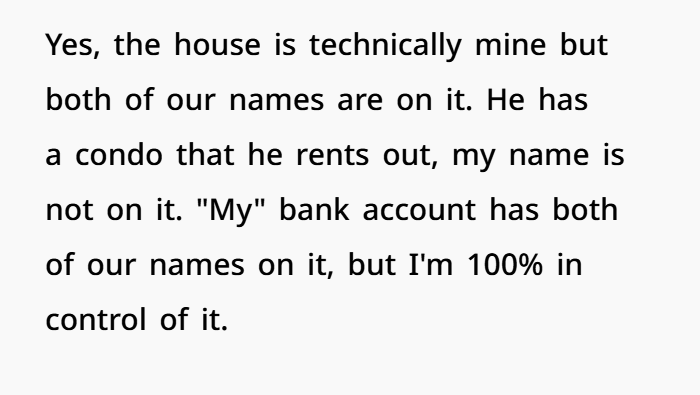

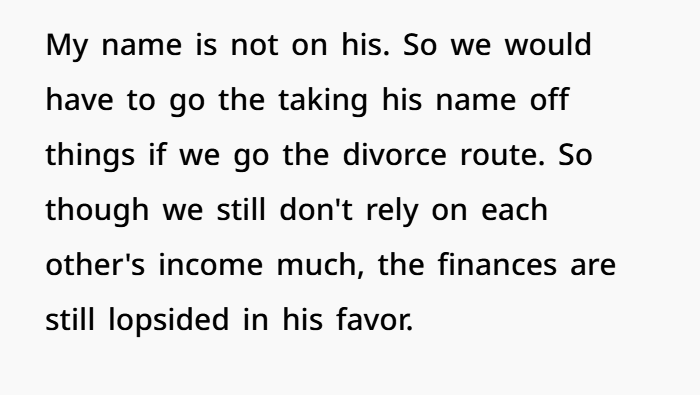

AITA for Telling My Husband It’s Life Insurance or Divorce After His Family’s Cancer Diagnosis?

A 45-year-old business owner became worried about her family’s financial future after seeing health problems affect someone close to her husband. Her brother-in-law was diagnosed with pancreatic cancer, and doctors suggested genetic testing because of a family history of serious illness. This made her think more about healthcare costs, income protection, and future financial security.

She had also seen her own mother struggle financially while caring for a seriously ill spouse. Because of those experiences, she believed having life insurance, disability insurance, and a strong financial plan was an important way to protect their family. She felt the conversation was about responsibility and preparation, not about money.

Her husband did not share the same concerns. He joked about the situation and said that if he became disabled, he would simply spend his time relaxing at home. His reaction frustrated her because she felt he was not taking important financial planning decisions seriously.

The woman suggested a legal arrangement where they would separate their finances on paper while continuing their relationship as before. She explained that her goal was to protect her business, personal assets, and long-term financial plans from possible medical expenses or unexpected challenges.

This situation shows why conversations about insurance, healthcare planning, and financial protection are important in relationships. Couples may have different views about money, but open communication and proper planning can help create a more secure future.

When Health Risks, Insurance, and Marriage Decisions Become Difficult Conversations

At first, this story may look like it is only about life insurance and money. But the deeper issue is much bigger.

It is about fear, planning for the future, and how two people handle uncertainty in different ways.

When serious illness affects a family, conversations about financial planning, health insurance, disability coverage, estate planning, and protecting assets can become very important. These topics are not always easy to discuss, but they can help families prepare for unexpected situations.

Why Health Concerns Can Create Fear

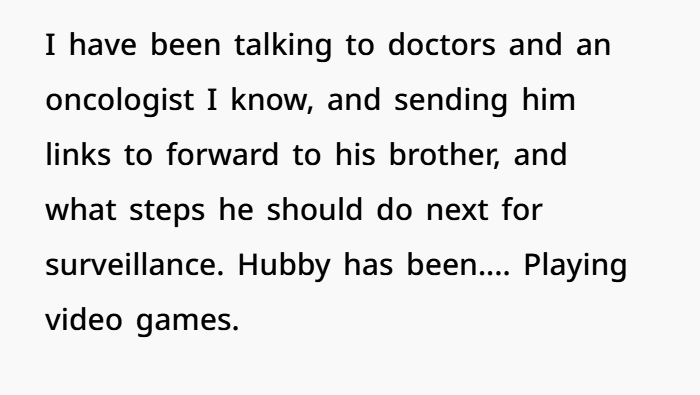

The wife in this situation is worried because her husband has a family history of a serious illness. His brother has been diagnosed with pancreatic cancer, and other family members have also experienced the disease.

When a family has a history of serious health conditions, doctors may recommend medical testing, regular checkups, or additional monitoring.

For someone who has already seen the effects of a major illness, these concerns can feel very real.

Her fear is not only about losing her husband. She is also thinking about what could happen afterward.

She may be worried about:

- Medical expenses

- Long-term care costs

- Loss of income

- Caregiving responsibilities

- Financial stress

- Protecting family savings

These are common concerns for families facing serious health risks.

Why Financial Planning Matters

Many people avoid talking about difficult financial topics until a crisis happens.

However, planning ahead can help families feel more prepared. Financial experts often encourage couples to discuss:

- Life insurance

- Disability insurance

- Emergency savings

- Estate planning

- Retirement planning

- Healthcare expenses

These conversations may feel uncomfortable, but they can help reduce stress during difficult times.

Planning does not mean expecting something bad to happen. It means being prepared if life takes an unexpected turn.

Different Ways People Handle Fear

The husband appears to respond differently. Instead of focusing on possible risks, he seems less worried about planning for them.

Some people may see this as avoiding responsibility. Others may see it as a way of coping with a scary situation.

People handle fear in different ways.

Some people prepare by making plans.

Others avoid thinking about worst-case situations because they feel overwhelming.

Neither reaction is unusual.

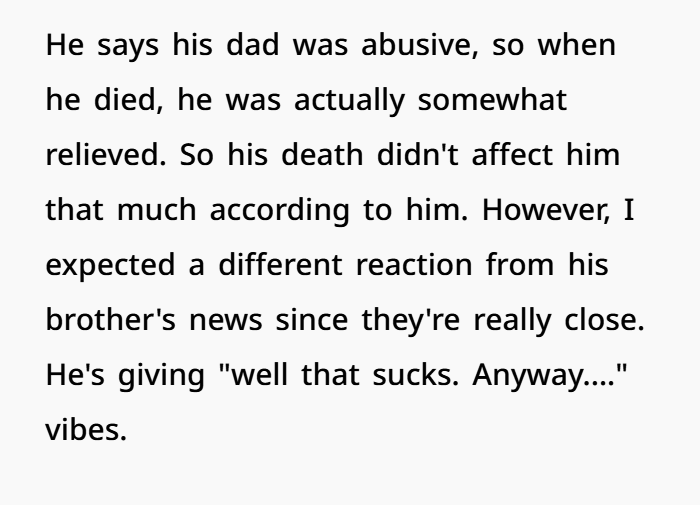

How Past Experiences Can Affect Emotions

Family experiences can influence how people deal with illness, loss, and fear.

The husband had a difficult relationship with his father, who was abusive. When his father passed away, he reportedly felt relief instead of sadness.

Growing up with painful experiences can affect how someone responds to emotional situations later in life.

Some people learn to protect themselves by:

- Avoiding difficult conversations

- Using humor during stressful moments

- Keeping emotional distance

- Trying not to think about painful possibilities

This does not always mean someone does not care. It may mean they process emotions differently.

The Real Problem May Be Communication

The disagreement may seem like it is about insurance, but the deeper issue is communication.

The wife may not simply be asking for an insurance policy. She may be saying:

“I want us to be prepared.”

“I want to protect our future.”

“I do not want to face a serious crisis without support.”

“I need to know we are a team.”

The husband may not simply be refusing insurance. He may be feeling:

“I do not want to live in fear.”

“I do not want to assume something bad will happen.”

“I want to enjoy life without constantly worrying.”

Both sides may have valid feelings, but they are focusing on different parts of the problem.

When Practical Problems Become Emotional Arguments

Many couples experience this type of conflict.

A practical topic, such as money or insurance, can become connected to deeper emotions.

For one person, insurance may represent:

- Love

- Responsibility

- Protection

- Planning

For another person, it may feel like:

- Fear

- Stress

- Accepting a negative future

Understanding these differences can help couples have better conversations.

Finding a Balanced Solution

Preparing for the future and enjoying the present can happen at the same time.

Buying insurance does not mean someone expects a tragedy.

Creating an emergency fund does not mean someone believes a crisis is coming.

Making a financial plan simply means being responsible.

At the same time, living with constant fear can also create stress. Couples need to find a balance between being prepared and enjoying their lives together.

The Importance of Respectful Conversations

Threats or emotional reactions can make difficult conversations even harder.

Instead of focusing only on the disagreement, couples can try discussing the feelings behind it.

Helpful questions may include:

- What are we both afraid of?

- How can we protect our future together?

- What financial steps make sense for our family?

- How can we support each other?

The goal should not be to win the argument. The goal should be understanding each other.

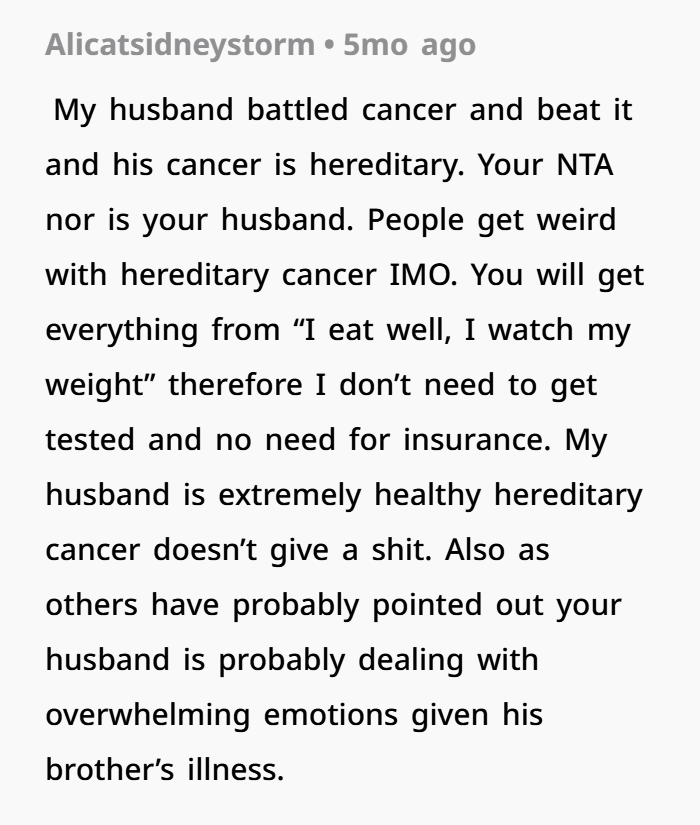

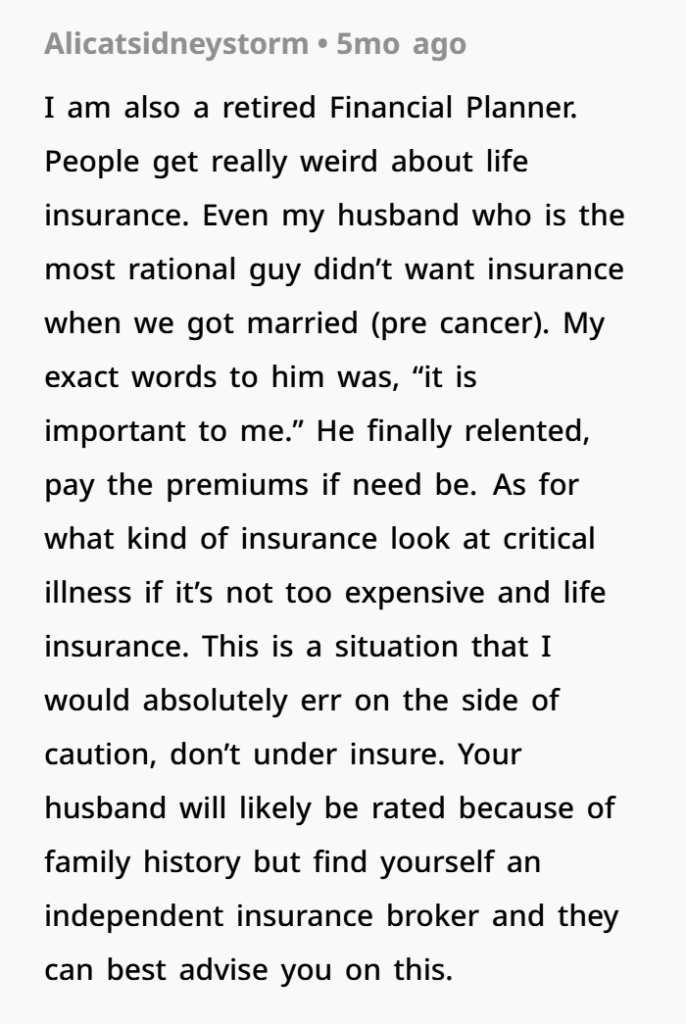

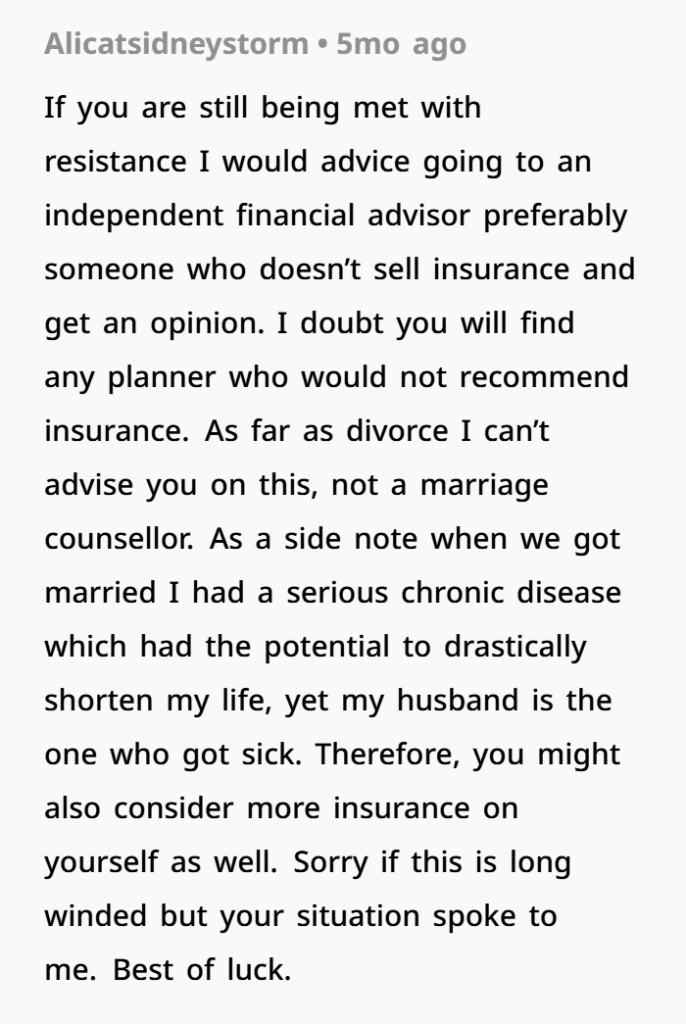

Top Comments From Readers

Final Thoughts

Health concerns, money decisions, and family history can create very emotional conversations.

One person may respond by planning, while another may respond by avoiding fear. Both reactions come from trying to handle uncertainty.

The strongest relationships are often built when couples stop fighting about the surface problem and start discussing the real emotions underneath.

Preparing for the future is an act of care, but so is supporting each other through difficult conversations.