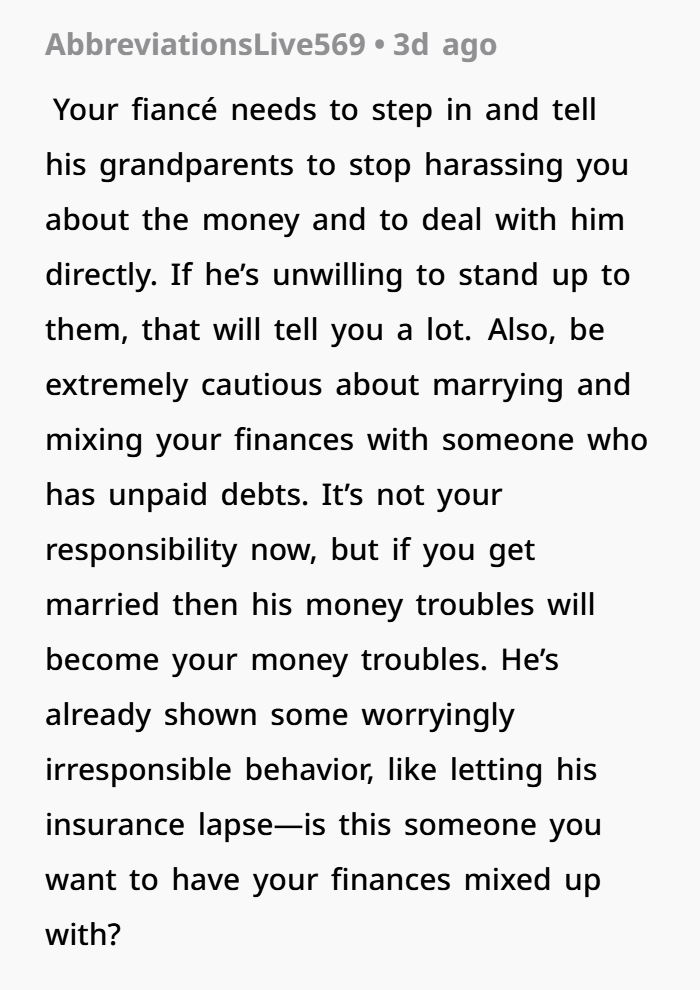

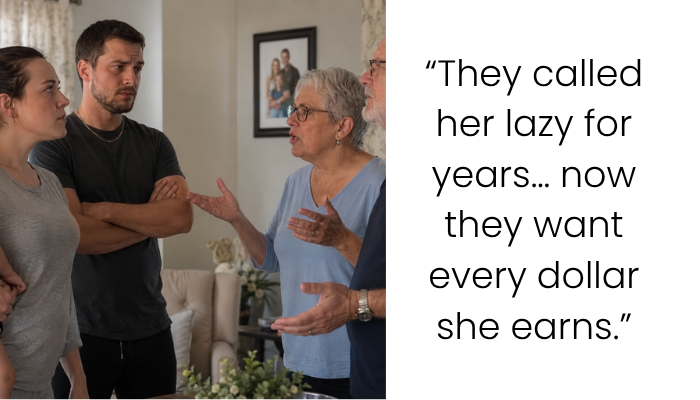

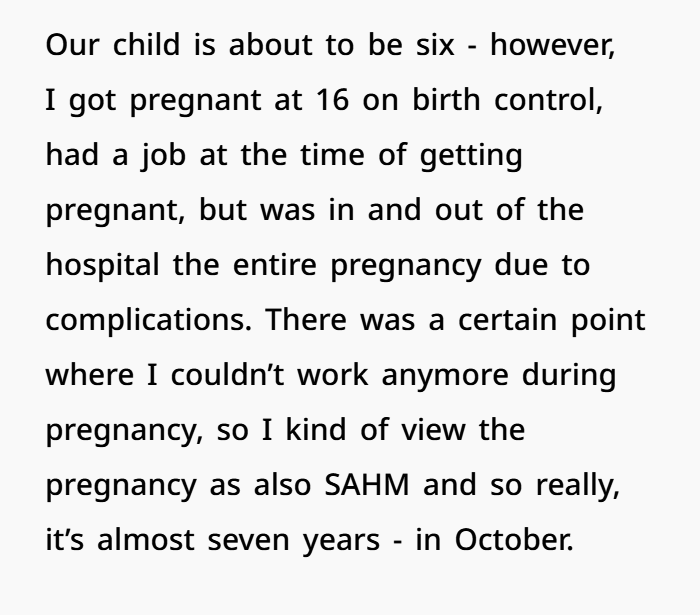

AITAH for Refusing to Use My Entire Paycheck to Repay My Fiancé’s Family?

Money problems can create stress in relationships, especially when one person feels responsible for a debt they did not create. In this story, a young mother shared her concerns about being expected to use her entire paycheck to help pay off financial problems connected to her fiancé’s debt.

The couple has been together since they were teenagers, but his grandparents were never fully supportive of their relationship. According to the woman, they often blamed her for financial struggles and believed she was preventing her fiancé from moving forward. They also judged her decision to stay home with their child.

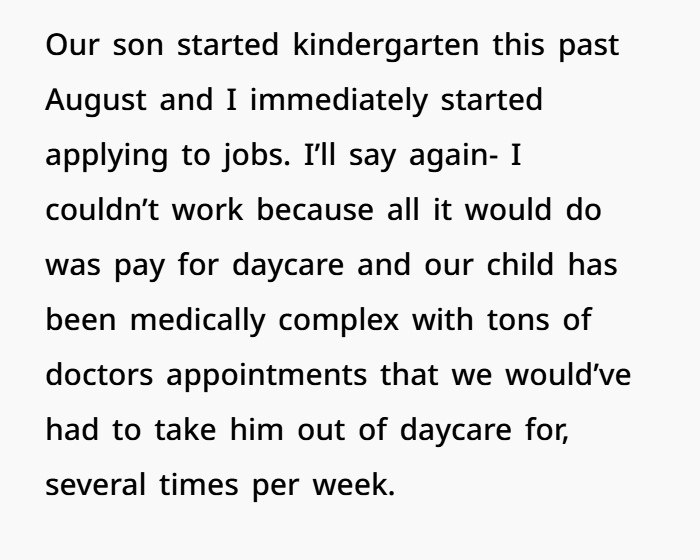

The woman explained that she became pregnant at 16 while working, but health problems during pregnancy forced her to leave her job. After their son was born, he needed regular medical care and many appointments. The couple decided that staying home was the best option because childcare costs would have been very expensive.

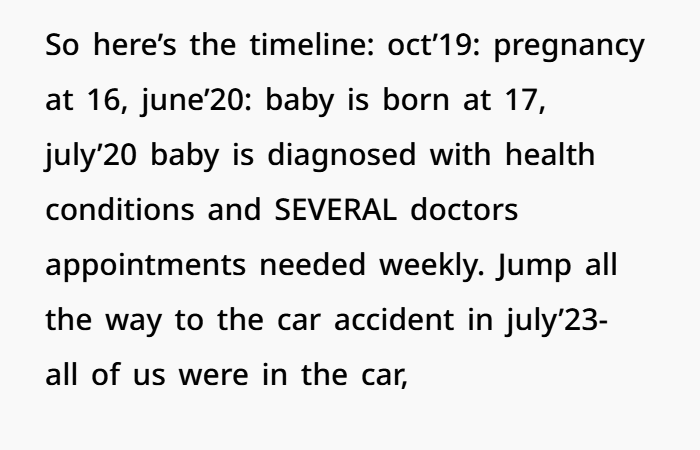

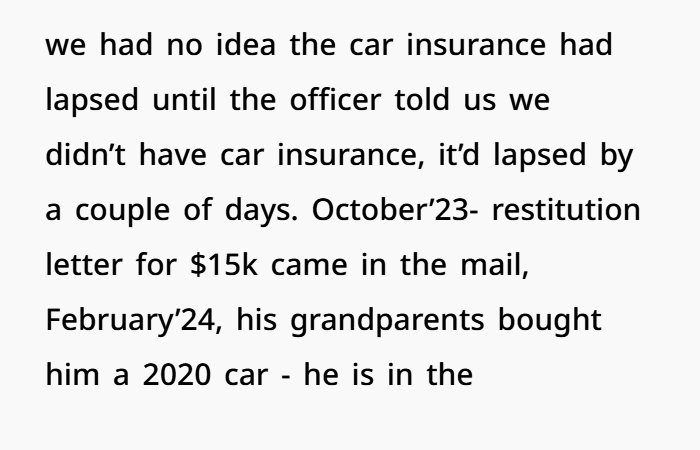

During that time, her fiancé had a financial problem involving a vehicle. She said he allowed the insurance to expire and later had an accident that created a large amount of debt. His grandparents helped pay the costs and provided another vehicle, with the expectation that he would repay them.

Now that the woman has started working again and earning income, she feels uncomfortable with the expectation that her full salary should go toward a debt she did not create. The situation has created questions about financial responsibility, family support, budgeting, and how couples should handle money decisions together. Open communication and clear financial planning are important when dealing with debt and shared expenses.

When Family Money Problems Create Relationship Stress

Money problems can be one of the hardest challenges for a family.

When debt, caregiving responsibilities, childcare costs, and family expectations all come together, even strong relationships can experience stress.

Stories like this connect with many people because they highlight a bigger conversation about unpaid work, financial pressure, and the value of caregiving.

The Hidden Cost of Being a Stay-at-Home Parent

Many people assume that staying home with children means someone is not contributing financially.

But that view often ignores the real work involved.

A stay-at-home parent may handle:

- Childcare

- Household responsibilities

- Medical appointments

- Daily routines

- Transportation needs

- Emotional support

This work has real value, even if it does not come with a traditional paycheck.

For families with children who have extra medical or care needs, the responsibilities can become even more demanding.

Professional childcare, home care support, and specialized services can be very expensive. In many cases, one parent staying home may be the most practical decision for the family.

Financial Problems Are Often More Complicated Than They Look

When a family experiences debt, it is usually caused by several factors, not just one decision.

Unexpected events can create major financial pressure, including:

- Medical expenses

- Transportation costs

- Legal fees

- Emergency situations

- Changes in employment

It is important to look at the full financial picture instead of blaming one person for every challenge.

Good financial planning means understanding where money problems came from and creating a realistic plan to move forward.

The Value of Unpaid Caregiving

Unpaid caregiving is often overlooked.

A parent caring for a child full-time provides services that families often pay others to provide.

Examples include:

- Babysitting

- Transportation

- Meal preparation

- Appointment management

- Daily care support

If families had to hire outside help for all of these tasks, the costs could be very high.

This is why many financial experts and family researchers recognize that caregiving has economic value.

Returning to Work After Years at Home

When a stay-at-home parent returns to work, it can be an important step toward financial independence.

A new job can help with:

- Household expenses

- Personal savings

- Career growth

- Long-term financial security

However, returning to work after years away can also be challenging.

Many parents face questions about balancing:

- Work responsibilities

- Childcare

- Family needs

- Relationship expectations

A healthy financial plan should consider everyone’s needs.

The Importance of Financial Independence

Money can affect relationships in many ways.

Healthy couples usually make financial decisions together. They discuss:

- Income

- Expenses

- Debt repayment

- Savings goals

- Future plans

Problems can happen when one person feels they have no control over their own money.

Financial independence does not mean someone does not care about their family. It means having the ability to make responsible decisions and feel secure.

Helping Family Members With Money

Many families help each other during difficult times.

Parents, grandparents, and relatives may provide financial support when someone faces an emergency.

Family support can be a wonderful thing, but money conversations should be clear.

Before accepting financial help, families can discuss:

- Is this a gift or a loan?

- Are there repayment expectations?

- What timeline is realistic?

- What happens if circumstances change?

Clear communication can prevent future misunderstandings.

The Difference Between Support and Pressure

Helping family financially can be a positive choice when everyone agrees.

However, pressure and guilt can make financial situations more stressful.

A healthy approach focuses on teamwork.

Instead of asking:

“Who is responsible for this problem?”

Families can ask:

“How can we solve this together?”

This change in mindset can reduce conflict and improve communication.

Why Couples Need Strong Boundaries

When extended family members become involved in money decisions, couples may experience extra stress.

Partners often need to work together to decide:

- What they can realistically afford

- How they will handle debt

- How much outside help they accept

- What financial goals matter most

A strong relationship requires both partners to feel heard and respected.

The Challenges of Young Parents

Becoming a parent at a young age can already be difficult.

When young parents also face healthcare needs, financial challenges, or caregiving responsibilities, the pressure can become much greater.

Many young families struggle with:

- Building careers

- Managing expenses

- Finding childcare

- Creating financial stability

Support and understanding can make a major difference.

Creating a Healthier Financial Future

There is no perfect solution for every family.

Every household has different needs, responsibilities, and challenges.

Some helpful steps include:

- Creating a realistic budget

- Building emergency savings

- Discussing financial goals openly

- Seeking professional financial advice when needed

- Respecting each person’s contribution

Both paid work and unpaid caregiving can support a family.

The Bigger Lesson

This type of situation is about more than money.

It is about recognizing the value of caregiving, understanding family finances, and creating relationships based on respect.

Financial challenges can be stressful, but they do not have to divide families.

With honest communication, clear boundaries, and shared goals, families can work toward greater financial stability and emotional well-being.

See The Comments Below